Previously we have written about “being digital” in the  context of shifting business models and approaches as we move from an analog world to a digital world. Underlying this change have been 3 significant tsunami waves of digitization in the communications arena over the past 30 years, underappreciated and unnoticed by almost all until after they had crashed onto the landscape:

context of shifting business models and approaches as we move from an analog world to a digital world. Underlying this change have been 3 significant tsunami waves of digitization in the communications arena over the past 30 years, underappreciated and unnoticed by almost all until after they had crashed onto the landscape:

- The WAN wave between 1983-1990 in the competitive long-distance market, continuing through the 1990s;

- The Data wave, itself a direct outgrowth of the first wave, began in the late 1980s with flat-rate local dial-up connections to ISPs and databases anywhere in the world (aka the Web);

- The Wireless wave beginning in the early 1990s and was a direct outgrowth of the latter two. Digital cellphones were based on the same technology as the PCs that were exploding with internet usage. Likewise, super-low-cost WAN pricing paved the way for one-rate, national pricing plans. Prices dropped from $0.50-$1.00 to less than $0.10. Back in 1996 we correctly modeled this trend before it happened.

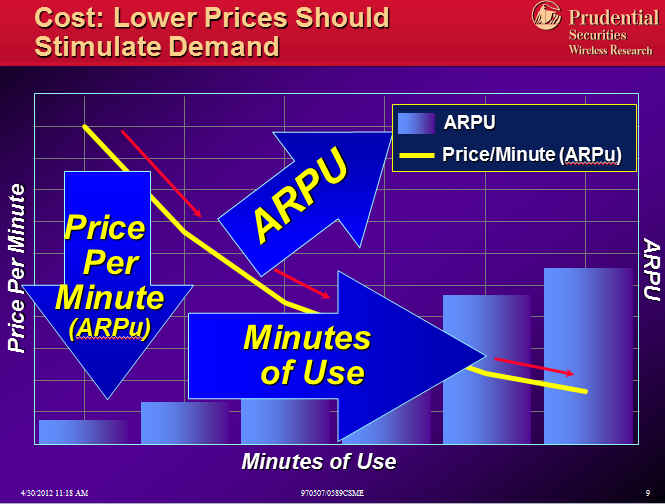

Each wave may have looked different, but they followed the same patterns, building on each other. As unit prices dropped 99%+ over a 10 year period unit demand exploded resulting in 5-25% total market growth. In other words, as ARPu dropped ARPU rose; u vs U, units vs Users. Elasticity.

Yet with each new wave, people remained unconvinced about demand elasticity. They were just incapable of pivoting from the current view and extrapolating to a whole new demand paradigm. Without fail demand exploded each time coming from 3 broad areas: private to public shift, normal price elasticity, and application elasticity.

- Private to Public Demand Capture. Monopolies are all about average costs and consumption, with little regard for the margin. As a result, they lose the high-volume customer who can develop their own private solution. This loss diminishes scale economies of those who remain on the public, shared network raising average costs; the network effect in reverse. Introducing digitization and competition drops prices and brings back not all, but a significant number of these private users. Examples we can point to are private data and voice networks, private radio networks, private computer systems, etc…that all came back on the public networks in the 1980s and 1990s. Incumbents can’t think marginally.

- Normal Price Elasticity. As prices drop, people will use more. It gets to the point where they forget how much it costs, since the relative value is so great. One thing to keep in mind is that lazy companies can rely too much on price and “all-you-can-eat” plans without regard for the real marginal price to marginal cost spread. The correct approach requires the right mix of pricing, packaging and marketing so that all customers at the margin feel they are deriving much more value than what they are paying for; thus generating the highest margins. Apple is a perfect example of this. Sprint’s famous “Dime” program was an example of this. The failure of AYCE wireless data plans has led wireless carriers to implement arbitrary pricing caps, leading to new problems. Incumbents are lazy.

- Application Elasticity. The largest and least definable component of demand is the new ways of using the lower cost product that 3rd parties drive into the ecosystem. They are the ones that drive true usage via ease of use and better user interfaces. Arguably they ultimately account for 50% of the new demand, with the latter 2 at 25% each. With each wave there has always been a large crowd of value-added

resellers and application developers that one can point to that more effectively ferret out new areas of demand. Incumbents move slowly.

resellers and application developers that one can point to that more effectively ferret out new areas of demand. Incumbents move slowly.

Demand generated via these 3 mechanisms soaked up excess supply from the digital tsunamis. In each case competitive pricing was arrived at ex ante by new entrants developing new marginal cost models by iterating future supply/demand scenarios. It is this ex ante competitive guess, that so confounds the rest of the market both ahead and after the event. That's why few people recognize that these 3 historical waves are early warning signs for the final big one. The 4th and final wave of digitization will occur in the mid-to-last mile broadband markets. But many remain skeptical of what the "demand drivers" will be. These last mile broadband markets are monopoly/duopoly controlled and have not yet realized price declines per unit that we’ve seen in the prior waves. Jim Crowe of Level3 recently penned a piece in Forbes that speaks to this market failure. In coming posts we will illustrate where we think bandwidth pricing is headed, as people remain unconvinced about elasticity, just as before. But hopefully the market has learned from the prior 3 waves and will understand or believe in demand forecasts if someone comes along and says last mile unit bandwidth pricing is dropping 99%. Because it will.