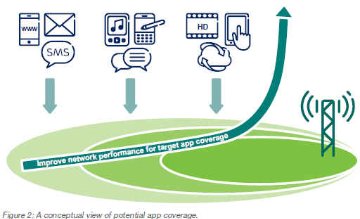

Given the smartphone’s ubiquity and our dependence on it, “App Coverage” (AC) is something confronting us every day, yet we know little about it. At the CCA Global Expo this week in San Antonio Glenn Laxdal of Ericsson spoke about “app coverage”, which the vendor first surfaced in 2013. AC is defined as, “the proportion of a network’s coverage that has sufficient performance to run a particular app at an acceptable quality level.” In other words the variety of demand from end-users for voice, data and video applications is outpacing the ability of carriers to keep up. According to Ericsson, monitoring and ensuring performance of app coverage is the next wave in LTE networks. Here’s a good video explaining AC in simple, visual terms.

Years, nay, decades ago I used to say coverage should be measured in 3 important ways:

Geographic (national vs regional vs local)

In/Outdoors (50+% loss indoors)

Frequency (double capex 1900 vs 700 mhz)

Each of these had specific supply/demand clearing implications across dozens of issues impacting balance sheets and P&L statements; ultimately determining winners and losers. They are principally why AT&T and Verizon today have 70% of subscribers (80% of enterprise customers) up from 55% just 5 years ago, 84% of total profit, and over 100% of industry free cash flow. Now we can add “applications” to that list. And it will only make it more challenging for competitors to wrestle share from the “duopoly”.

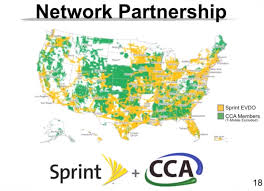

Cassidy Shield of Alcatel-Lucent, further stated that fast follower strategies to the duopoly would likely fail; implying that radical rethinking was necessary. Some of that came quickly in the form of Masayoshi Son’s announcement of a broad partnership with NetAmerica and members of CCA for preferred roaming, concerted network buildout and sharing of facilities and device purchase agreements. This announcement came two weeks after Son visited Washington DC and laid out Sprint’s vision for a new, more competitive wireless future in America.

The conference concluded with a panel of CEOs hailing Sprint’s approach, which Son outlined here, as one of benevolent dictator (perhaps not the best choice of words) and exhorting the label partner, partner, partner; something that Terry Addington of MobileNation has said has taken way too long. Even then the panel agreed that pulling off partnerships will be challenging.

The Good & Bad of Wireless

Wireless is great because it is all things to all people, and that is what makes it bad too. Planning for and accounting how users will access the network is very challenging across a wide user base. There are fundamentally different “zones” and contexts in which different apps can be used and they often conflict with network capacity and performance. I used to say that one could walk and also hang upside down from a tree and talk, but you couldn’t “process data” doing those things. Of course the smartphone changed all that and people are accessing their music apps, location services, searches, purchases, and watching video from anywhere; even hanging upside down in trees.

Today voice, music and video consume 12, 160 and 760 kpbs of bandwidth, respectively, on average. Tomorrow those numbers might be 40, 500, 1500, and that’s not even taking into account “upstream” bandwidth which will be even more of a challenge for service providers to provision when consumers expect more 2-way collaboration everywhere. The law of wireless gravity, which states bits will seek out fiber/wire as quickly and cheaply as possible, will apply, necessitating sharing of facilities (wireless and wired), heterogeneous network (Hetnet), and aggressive wifi offload approaches; even consumers will be shared in the form of managed services across communities of users (known today as OTT). The show agenda included numerous presentations on distributed antennae networks and wifi offload applied to the rural coverage challenge.

Developing approaches ex ante to anticipate demand is even more critical if carriers want to play major roles in the internet of things, unified (video) communications and the connected car. As Ericsson states in its whitepaper,

“App coverage integrates all aspects of network performance – including radionetwork throughput and latency, capacity, as well as the performance of the backhaul, packetcore and the content-delivery networks. Ultimately, managing app coverage and performance demands a true end-to-end approach to designing, building and running mobile networks.”

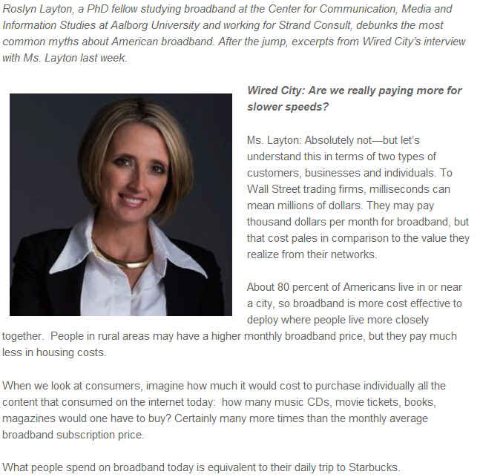

The current debate over the state of America's broadband services and over the future of the internet is like a 3-ring circus or 3 different monarchists debating democracy. In other words an ironic and tragically humorous debate between monopolists, be they ultra-conservative capitalists, free-market libertarians, or statist liberals. Their conclusions do not provide a cogent path to solving the single biggest socio-political-economic issue of our time due to pre-existing biases, incorrect information, or incomplete/wanting analysis. Last week I wrote about Google's conflicts and paradoxes on this issue. Over the next few weeks I'll expand on this perspective, but today I'd like to respond to a Q&A, Debunking Broadband's Biggest Myths, posted on Commercial Observer, a NYC publication that deals with real estate issues mostly and has recently begun a section called Wired City, dealing with a wide array of issues confronting "a city's" #1 infrastructure challenge. Here's my debunking of the debunker.

To put this exchange into context, the US led the digitization revolutions of voice (long-distance, touchtone, 800, etc..), data (the internet, frame-relay, ATM, etc...) and wireless (10 cents, digital messaging, etc...) because of pro-competitive, open access policies in long-distance, data over dial-up, and wireless interconnect/roaming. If Roslyn Layton (pictured below) did not conveniently forget these facts or does not understand both the relative and absolute impacts on price and infrastructure investment then she would answer the following questions differently:

Real Reason/Answer: our bandwidth is 20-150x overpriced on a per bit basis because we disconnected from moore's and metcalfe's laws 10 years ago, due to the Telecom Act, then special access "de"regulation, then Brand-X or shutting down equal access for broadband. This rate differential is shown in the discrepancy between rates we pay in NYC and what Google charges in KC, as well as the difference in performance/price of 4G and wifi. It is great Roslyn can pay $3-5 a day for Starbucks. Most people can't (and shouldn't have to) just for a cup a Joe that you can make at home for 10-30 cents.

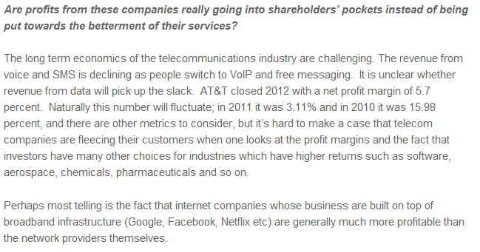

Real Reason/Answer: Because of their vertical business models, carriers are not well positioned to generate high ROI on rapidly depreciating technology and inefficient operating expense at every layer of the "stack" across geographically or market segment constrained demand. This is the real legacy of inefficient monopoly regulation. Doing away with regulation, or deregulating the vertical monopoly, doesn’t work. Both the policy and the business model need to be approached differently. Blueprints exist from the 80s-90s that can help us restructure our inefficient service providers. Basically, any carrier that is granted a public ROW (right of way) or frequency should be held to an open access standard in layer 1. The quid pro quo is that end-points/end-users should also have equal or unhindered access to that network within (economic and aesthetic) reason. This simple regulatory fix solves 80% of the problem as network investments scale very rapidly, become pervasive, and can be depreciated quickly.

Real Reason/Answer: Quasi monopolies exist in video for the cable companies and in coverage/standards in frequencies for the wireless companies. These scale economies derived from pre-existing monopolies or duopolies granted by and maintained to a great degree by the government. The only open or equal access we have left from the 1980s-90s (the drivers that got us here) is wifi (802.11) which is a shared and reusable medium with the lowest cost/bit of any technology on the planet as a result. But other generative and scalabeable standards developed in the US or with US companies at the same time, just like the internet protocol stacks, including mobile OSs, 4G LTE (based on CDMA/OFDM technology), OpenStack/Flow that now rule the world. It's very important to distinguish which of these are truly open or not.

Real Reason/Answer: The 3rd of the population who don't have/use broadband is as much because of context and usability, whether community/ethnicity, age or income levels, as cost and awareness. If we had balanced settlements in the middle layers based on transaction fees and pricing which reflect competitive marginal cost, we could have corporate and centralized buyers subsidizing the access and making it freely available everywhere for everyone. Putting aside the ineffective debate between bill and keep and 2-sided pricing models and instead implementing balanced settlement exchange models will solve the problem of universal HD tele-work, education, health, government, etc… We learned in the 1980s-90s from 800 and internet advertising that competition can lead to free, universal access to digital "economies". This is the other 20% solution to the regulatory problem.

Real Reason/Answer: The real issue here is that America led the digital information revolution prior to 1913 because it was a relatively open and competitive democracy, then took the world into 70 years of monopoly dark ages, finally breaking the shackles of monopoly in 1983, and then leading the modern information revolution through the 80s-90s. The US has now fallen behind in relative and absolute terms in the lower layers due to consolidation and remonopolization. Only the vestiges of pure competition from the 80s-90s, the horizontally scaled "data" and "content" companies like Apple, Google, Twitter and Netflix (and many, many more) are pulling us along. The vertical monopolies stifle innovation and the generative economic activity we saw in those 2 decades. The economic growth numbers and fiscal deficit do not lie.

Back in 1998 I wrote, “if you want to break up the Microsoft software monopoly then break up the Baby Bell last-mile access monopoly.” Market driven broadband competition and higher-capacity digital wireless networks gave rise to the iOS and Android operating systems over the following decade which undid the Windows monopoly. The 2013 redux to that perspective is, once again, “if you want to break up the Google search monopoly then break up the cable/telco last mile monopolies.”

Google is an amazing company, promoting the digital pricing and horizontal service provider spirit more than anyone. But Google is motivated by profit and will seek to grow that profit as best it can, even if contrary to founding principles and market conditions that fueled its success (aka net neutrality or equal access). Now that Google is getting into the lower layers in the last mile they are running into paradoxes and conflicts over net neutrality/equal access and in danger of becoming just another vertical monopoly. (Milo Medin provides an explanation in the 50th minute in this video, but it is self-serving, disingenuous and avoids confronting the critical issue for networks going forward.)

Contrary to many people’s beliefs, the upper and lower layers have always been inextricably interdependent and nowhere was this more evident than with the birth of the internet out of the flat-rate dial-up networks of the mid to late 1980s (a result of dial-1 equal access). The nascent ISPs that scaled in the 1980s on layer 1-2 data bypass networks were likewise protected by Computers II-III (aka net neutrality) and benefited from competitive (WAN) transport markets.

Few realize or accept the genesis of Web 1.0 (W1.0) was the break-up of AT&T in 1983. Officially birthed in 1990 it was an open, 1-way store and forward database lookup platform on which 3 major applications/ecosystems scaled beginning in late 1994 with the advent of the browser: communications (email and messaging), commerce, and text and visual content. Even though everything was narrowband, W1.0 began the inexorable computing collapse back to the core, aka the cloud (4 posts on the computing cycle and relationship to networks). The fact that it was narrowband didn't prevent folks like Mark Cuban and Jeff Bezos from envisioning and selling a broadband future 10 years hence. Regardless, W1.0 started collapsing in 1999 as it ran smack into an analog dial-up brick wall. Google hit the bigtime that year and scaled into the early 2000s by following KISS and freemium business model principles. Ironically, Google’s chief virtue was taking advantage of W1.0’s primary weakness.

Web 2.0 grew out of the ashes of W1.0 in 2002-2003. W2.0 both resulted from and fueled the broadband (BB) wars starting in the late 1990s between the cable (offensive) and telephone (defensive) companies. BB penetration reached 40% in 2005, a critical tipping point for the network effect, exactly when YouTube burst on the scene. Importantly, BB (which doesn't have equal access, under the guise of "deregulation") wouldn’t have occurred without W1.0 and the above two forms of equal access in voice and data during the 1980s-90s. W2.0 and BB were mutually dependent, much like the hardware/software Wintel model. BB enabled the web to become rich-media and mostly 2-way and interactive. Rich-media driven blogging, commenting, user generated content and social media started during the W1.0 collapse and began to scale after 2005.

“The Cloud” also first entered people’s lingo during this transition. Google simultaneously acquired YouTube in the upper layers to scale its upper and lower layer presence and traffic and vertically integrated and consolidated the ad exchange market in the middle layers during 2006-2008. Prior to that, and perhaps anticipating lack of competitive markets due to "deregulation" of special access, or perhaps sensing its own potential WAN-side scale, the company secured low-cost fiber rights nationwide in the early 2000s following the CLEC/IXC bust and continued throughout the decade as it built its own layer 2-3 transport, storage, switching and processing platform. Note, the 2000s was THE decade of both vertical integration and horizontal consolidation across the board aided by these “deregulatory” political forces. (Second note, "deregulatory" should be interpreted in the most sarcastic and insidious manner.)

Web 3.0 began officially with the iPhone in 2007. The smartphone enabled 7x24 and real-time access and content generation, but it would not have scaled without wifi’s speed, as 3G wireless networks were at best late 1990s era BB speeds and didn’t become geographically ubiquitous until the late 2000s. The combination of wifi (high speeds when stationary) and 3G (connectivity when mobile) was enough though to offset any degradation to user experience. Again, few appreciate or realize that W3.0 resulted from two additional forms of equal access, namely cellular A/B interconnect from the early 1980s (extended to new digital PCS entrants in the mid 1990s) and wifi’s shared spectrum. One can argue that Steve Jobs single-handedly resurrected equal access with his AT&T agreement ensuring agnostic access for applications. Surprisingly, this latter point was not highlighted in Isaacson's excellent biography. Importantly, we would not have had the smartphone revolution were it not for Jobs' equal access efforts.

W3.0 proved that real-time, all the time "semi-narrowband" (given the contexts and constraints around the smartphone interface) trumped store and forward "broadband" on the fixed PC for 80% of people’s “web” experience (connectivity and interaction was more important than speed), as PC makers only realized by the late 2000s. Hence the death of the Wintel monopoly, not by government decree, but by market forces 10 years after the first anti-trust attempts. Simultaneously, the cloud became the accepted processing model, coming full circle back to the centralized mainframe model circa 1980 before the PC and slow-speed telephone network led to its relative demise. This circularity further underscores not only the interplay between upper and lower layers but between edge and core in the InfoStack. Importantly, Google acquired Android in 2005, well before W3.0 began as they correctly foresaw that small-screens and mobile data networks would foster the development of applications and attendant ecosystems would intrude on browser usage and its advertising (near) monopoly.

Web 4.0 is developing as we speak and no one is driving it and attempting to influence it more with its WAN-side scale than Google. W4.0 will be a full-duplex, 2-way, all-the time, high-definition application driven platform that knows no geographic or market segment boundaries. It will be engaging and interactive on every sensory front; not just those in our immediate presence, but everywhere (aka the internet of things). With Glass, Google is already well on its way to developing and dominating this future ecosystem. With KC Fiber Google is illustrating how it should be priced and what speeds will be necessary. As W4.0 develops the cloud will extend to the edge. Processing will be both centralized and distributed depending on the application and the context. There will be a constant state of flux between layers 1 and 3 (transport and switching), between upper and lower layers, between software and hardware at every boundary point, and between core and edge processing and storage. It will dramatically empower the end-user and change our society more fundamentally than what we’ve witnessed over the past 30 years. Unfortunately, regulators have no gameplan on how to model or develop policy around W4.0.

The missing pieces for W4.0 are fiber based and super-high capacity wireless access networks in the lower layers, settlement exchanges in the middle layers, and cross-silo ecosystems in the upper layers. Many of these elements are developing in the market naturally: big data, hetnets, SDN, openflow, open OS' like Android and Mozilla, etc… Google’s strategy appears consistent and well-coordinated to tackle these issues; if not far ahead of others. But its vertically integrated service provider model and stance on net neutrality in KC is in conflict with the principles that so far have led to its success.

Google is buying into the vertical monopoly mindset to preserve its profit base instead of teaching regulators and the markets about the virtues of open or equal access across every layer and boundary point (something clearly missing from Tim Wu's and Bob Atkinson's definitions of net neutrality). In the process it is impeding the development of W4.0. Governments could solve this problem by simply conditioning any service provider with access to a public right of way or frequency to equal access in layers 1 and 2; along with a quid pro quo that every user has a right to access unhindered by landlords and local governments within economic and aesthetic reason. (The latter is a bone we can toss all the lawyers who will be looking for new work in the process of simpler regulations.) Google and the entire market will benefit tremendously by this approach. Who will get there first? The market (Google or MSFT/AAPL if the latter are truly hungry, visionary and/or desperate) or the FCC? Originally hopeful, I’ve become less sure of the former over the past 12 months. So we may be reliant on the latter.

Since I began covering the sector in 1990, I’ve been waiting for Big Bang II.An adult flick?No, the sequel to Big Bang (aka the breakup of MaBell and the introduction of equal access) was supposed to be the breakup of the local monopoly.Well thanks to the Telecom Act of 1996 and the well-intentioned farce that it was, that didn’t happen and equal access officially died (equal access RIP) in 2005 with the Supreme Court's Brand-X decision vs the FCC. If it died, then we saw a resurrection that few noticed.

I am announcing that Equal Access is alive and well, albeit in a totally unexpected way.Thanks to Steve Jobs’ epochal demands put on AT&T to counter its terrible 2/3G network coverage and throughput, every smartphone has an 802.11 (WiFi) backdoor built-in.Together with the Apple and Google operating systems being firmly out of carriers’ hands and scaling across other devices (tablets, etc…) a large ecosystem of over-the-top (OTT), unified communications and traffic offloading applications is developing to attack the wireless hegemony.

First, a little history. Around the time of AT&T's breakup the government implemented 2 forms of equal access. Dial-1 in long-distance made marketing and application driven voice resellers out of the long-distance competitors. The FCC also mandated A/B cellular interconnect to ensure nationwide buildout of both cellular networks. This was extended to nascent PCS providers in the early to mid 1990s leading to dramatic price declines and enormous demand elasticities. Earlier, the competitive WAN/IXC markets of the 1980s led to rapid price reductions and to monopoly (Baby Bell or ILEC) pricing responses that created the economic foundations of the internet in layers 1 and 2; aka flat-rate or "unlimited" local dial-up. The FCC protected the nascent ISP's by preventing the Bells from interfering at layer 2 or above. Of course this distinction of MAN/LAN "net-neutrality" went away with the advent of broadband, and today it is really just about WAN/MAN fights between the new (converged) ISPs or broadband service providers like Comcast, Verizon, etc... and the OTT or content providers like Google, Facebook, Netflix, etc...

(Incidentally, the FCC ironically refers to edge access providers, who have subsumed the term ISPs or "internet service providers", as "core" providers, while the over-the-top (OTT) messaging, communications, e-commerce and video streaming providers, who reside at the real core or WAN, are referred to as "edge" providers. There are way, way too many inconsistencies for truly intelligent people to a) come up with and b) continue to promulgate!)

But a third form of equal access, this one totally unintentioned, happened with 802.11 (WiFi) in the mid 1990s. The latter became "nano-cellular" in that power output was regulated limiting hot-spot or cell-size to ~300 feet. This had the impact of making the frequency band nearly infinitely divisible. The combination was electric and the market, unencumbered by monopoly standards and scaling along with related horizontal layer 2 data technologies (ethernet), quickly seeded itself. It really took off when Intel built WiFi capability directly into it's Centrino chips in the early 2000s. Before then computers could only access WiFi with usb dongles or cables tethered to 2G phones

Cisco just forecast that 50% of all internet traffic will be generated from 802.11 (WiFi) connected devices.Given that 802.11’s costs are 1/10th those of 4G something HAS to give for the communications carrier.We’ve talked about them needing to address the pricing paradox of voice and data better, as well as the potential for real obviation at the hands of the application and control layer worlds.While they might think they have a near monopoly on the lower layers, Steve Job’s ghost may well come back to haunt them if alternative access networks/topologies get developed that take advantage of this equal access. For these networks to happen they will need to think digital, understand, project and foster vertically complete systems and be able to turn the "lightswitch on" for their addressable markets.

Counter-intuitive thinking often leads to success.That’s why we practice and practice so that at a critical moment we are not governed by intuition (chance) or emotion (fear).No better example of this than in skiing; an apt metaphor this time of year.Few self-locomoted sports provide for such high risk-reward requiring mental, physical and emotional control.To master skiing one has to master a) the fear of staying square (looking/pointing) downhill, b) keeping one’s center over (or keeping forward on) the skis, and c) keeping a majority of pressure on the downhill (or danger zone) ski/edge.Master these 3 things and you will become a marvelous skier.Unfortunately, all 3 run counter to our intuitions driven by fear and safety of the woods at the side of the trail, leaning back and climbing back up hill. Overcoming any one is tough.

What got me thinking about all this was a Vint Cerf (one of the godfathers of the Internet) Op-Ed in the NYT this morning which a) references major internet access policy reports and decisions, b) mildly supports the notion of the Internet as a civil not human right, and c) trumpets the need for engineers to put in place controls that protect people’s civil (information) rights.He is talking about policy and regulation from two perspectives, business/regulatory and technology/engineering, which is confusing.In the process he weighs in, at a high level, on current debates over net neutrality, SOPA, universal service and access reform, from his positions at Google and IEEE and addresses the rights and governance from an emotional and intuitive sense.

Just as with skiing, let’s look at the issues critically, unemotionally and counter-intuitively.We can’t do it all in this piece, so I will establish an outline and framework (just like the 3 main ways to master skiing) and we’ll use that as a basis in future pieces to expound on the above debates and understand corporate investment and strategy as 2012 unfolds.

First, everyone should agree that the value of networks goes up geometrically with each new participant.It’s called Metcalfe’s law, or Metcalfe’s virtue.Unfortunately people tend to focus on scale economies and cost of networks; rarely the value.It is hard to quantify that value because most have a hard time understanding elasticity and projecting unknown demand.Further few rarely distinguish marginal from average cost.The intuitive thing for most to focus on is supply, because people fear the unknown (demand).

Second, everyone needs to realize that there is a fundamental problem with policy making in that (social) democrats tend to support and be supported by free market competitors, just as (conservative) republicans have a similar relationship with socialist monopolies.Call it the telecom regulatory paradox.This policy paradox is a function of small business vs big business, not either sides’ political dogma; so counter-intuitive and likely to remain that way.

Third, the internet was never open and free.Web 1.0 resulted principally from a judicial action and a series of regulatory access frameworks/decisions in the mid to late 1980s that resulted in significant unintended consequences in terms of people's pricing perception.Markets and technology adapted to and worked around inefficient regulations.Policy makers did not create or herald the internet, wireless and broadband explosions of the past 25 years.But in trying to adjust or adapt past regulation they are creating more, not less, inefficiency, no matter how well intentioned their precepts.Accept it as the law of unintended consequences.People feel more comfortable explaining results from intended actions than something unintended or unexplainable.

So, just like skiing, we’ve identified 3 principles of telecoms and information networks that are counter-intuitive or run contrary to accepted notions and beliefs.When we discuss policy debates, such as net neutrality or SOPA, and corporate activity such as AT&T’s aborted merger with T-Mobile or Verizon’s spectrum and programming agreement with the cable companies, we will approach and explain them in the context of Metcalfe’s Virtue (demand vs supply), the Regulatory Paradox (vertical vs horizontal orientation; not big vs small), and the law of unintended consequences (particularly what payment systems stimulate network investment).Hopefully the various parties involved can utilize this approach to better understand all sides of the issue and come to more informed, balanced and productive decisions.

Vint supports the notion of a civil right (akin to universal service) for internet access.This is misguided and unachievable via regulatory edict/taxation.He also argues that there should be greater control over the network.This is disingenuous in that he wants to throttle the open-ness that resulted in his godchild’s growth. But consider his positions at Google and IEEE. A “counter-intuitive” combination of competition, horizontal orientation and balanced payments is the best approach for an enjoyable and rewarding experience on the slopes of the internet and, who knows, ultimately and counterintuitively offering free access to all.The regulators should be like the ski patrol to ensure the safety of all. Ski school is now open.

coverage is the next wave in LTE networks. Here’s a good video explaining AC in

coverage is the next wave in LTE networks. Here’s a good video explaining AC in  Cassidy Shield of Alcatel-Lucent, further stated that

Cassidy Shield of Alcatel-Lucent, further stated that

w self-locomoted sports provide for such high risk-reward requiring mental, physical and emotional control.

w self-locomoted sports provide for such high risk-reward requiring mental, physical and emotional control. intuitions driven by

intuitions driven by  the need for engineers to put in place controls that protect people’s civil (information) rights.

the need for engineers to put in place controls that protect people’s civil (information) rights. we discuss policy debates, such as net neutrality or SOPA, and corporate activity such as AT&T’s aborted merger with T-Mobile or Verizon’s spectrum and programming agreement with the cable companies, we will approach and explain them in the context of Metcalfe’s Virtue (demand vs supply), the Regulatory Paradox (vertical vs horizontal orientation; not big vs small), and

we discuss policy debates, such as net neutrality or SOPA, and corporate activity such as AT&T’s aborted merger with T-Mobile or Verizon’s spectrum and programming agreement with the cable companies, we will approach and explain them in the context of Metcalfe’s Virtue (demand vs supply), the Regulatory Paradox (vertical vs horizontal orientation; not big vs small), and