The US has lacked a telecom network visionary for nearly 2 decades. There have certainly been strong and capable leaders, such as John Malone who not only predicted but brought about the 500 channel LinearTV model. But there hasn’t been someone like Bill McGowan who broke up AT&T or Craig McCaw who first had the vision to build a national, seamless wireless network, countering decades of provincial, balkanized thinking. Both of them fundamentally changed the thinking around public service provider networks.

But with a strong message to the markets in Washington DC on March 11 from Masayoshi Son, Sprint’s Chairman, the 20 year wait may finally be over. Son did what few have been capable of doing over the past 15-20 years since McGowan exited stage left and McCaw sold out to MaBell: telling it like it is. The fact is that today’s bandwidth prices are 20-150x higher than they should be with current technology.

This is no one’s fault in particular and in fact to most people (even informed ones) all measures of performance-to-price compared to 10 or 20 years ago look great. But, as Son illustrated, things could be much, much better. And he’s willing to make a bet on getting the US, the most advanced and heterogeneous society, back to a leadership role with respect to the ubiquity and cost of bandwidth. To get there he needs more scale and one avenue is to merge with T-Mobile.

There have been a lot of naysayers as to the possibility of a Sprint-T-Mo hookup, including leaders at the FCC. But don’t count me as one; it needs to happen. Initially skeptical when the rumors first surfaced in December, I quickly reasoned that a merger would be the best outcome for the incentive auctions. A merger would eliminate spectrum caps as a deterrent to active bidding and maximize total proceeds. It would also have a better chance of developing a credible third competitor with equal geographic reach. Then in January the FCC and DoJ came out in opposition to the merger.

In February, though, Comcast announced the much rumored merger with TW and Son jumped on the opportunity to take his case for merging to a broader stage. He did so in front of a packed room of 300 communications pundits, press and politicos at the US Chamber of Commerce’s prestigious Hall of Flags; a poignant backdrop for his own rags to riches story. Son’s frank honesty about the state of broadband for the American public vs the rest of the world, as well as Sprint’s own miserable current performance were impressive. It’s a story that resonates with my America’s Bandwidth Deficit presentation.

Here are some reasons the merger will likely pass:

The FCC can’t approve one horizontal merger (Comcast/TW) that brings much greater media concentration and control over content distribution, while disallowing a merger of two small players (really irritants as far as AT&T and Verizon are concerned).

Son has a solid track record of disruption and doing what he says.

The technology and economics are in his favor.

The vertically integrated service provider model will get disrupted faster and sooner as Sprint will have to think outside the box, partner, and develop ecosystems that few in the telecom industry have thought about before; or if they have, they’ve been constrained by institutional inertia and hidebound by legacy regulatory and industry siloes.

Here are some reasons why it might not go through:

The system is fundamentally corrupt. But the new FCC Chairman is cast from a different mold than his predecessors and is looking to make his mark on history.

The FCC shoots itself in the foot over the auctions. Given all the issues and sensitivities around incentive auctions the FCC wants this first one to succeed as it will serve as a model for all future spectrum refarming issues.

The FCC and/or DoJ find in the public interest that the merger reduces competition. But any analyst can see that T-Mo and Sprint do not have sustainable models at present on their own; especially when all the talk recently in Barcelona was already about 5G.

Personally I want Son’s vision to succeed because it’s the vision I had in 1997 when I originally brought the 2.5-2.6 (MMDS) spectrum to Sprint and later in 2001 and 2005 when I introduced Telcordia’s 8x8 MIMO solutions to their engineers. Unfortunately, past management regimes at Sprint were incapable of understanding the strategies and future vision that went along with those investment and technology pitches. Son has a different perspective (see in particular minute 10 of this interview with Walt Mossberg) with his enormous range of investments and clear understanding of price elasticity and the marginal cost of minutes and bits.

To be successful Sprint’s strategy will need to be focused, but at the same time open and sharing in order to simultaneously scale solutions across the three major layers of the informational stack (aka the InfoStack):

upper (application and content)

middle (control)

lower (access and transport)

This is the challenge for any company that attempts to disrupt the vertically integrated telecom or LinearTV markets; the antiquated and overpriced ones Son says he is going after in his presentation. But the US market is much larger and more robust than the rest of the world, not just geographically, but also from a 360 degree competitive perspective where supply and demand are constantly changing and shifting.

Ultimate success may well rest in the control layer, where Apple and Google have already built up formidable operating systems which control vastly profitably settlement systems across multiple networks. What few realize is that the current IP stack does not provide price signals and settlement systems that clear supply and demand between upper and lower layers (north-south) or between networks (east-west) in the newly converged “informational” stack of 1 and 2-way content and communications.

If Sprint’s Chairman realizes this and succeeds in disrupting those two markets with his strategy then he certainly will be seen as a visionary on par with McGowan and McCaw.

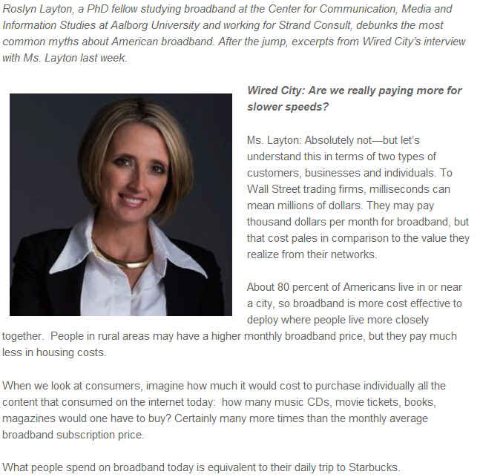

The current debate over the state of America's broadband services and over the future of the internet is like a 3-ring circus or 3 different monarchists debating democracy. In other words an ironic and tragically humorous debate between monopolists, be they ultra-conservative capitalists, free-market libertarians, or statist liberals. Their conclusions do not provide a cogent path to solving the single biggest socio-political-economic issue of our time due to pre-existing biases, incorrect information, or incomplete/wanting analysis. Last week I wrote about Google's conflicts and paradoxes on this issue. Over the next few weeks I'll expand on this perspective, but today I'd like to respond to a Q&A, Debunking Broadband's Biggest Myths, posted on Commercial Observer, a NYC publication that deals with real estate issues mostly and has recently begun a section called Wired City, dealing with a wide array of issues confronting "a city's" #1 infrastructure challenge. Here's my debunking of the debunker.

To put this exchange into context, the US led the digitization revolutions of voice (long-distance, touchtone, 800, etc..), data (the internet, frame-relay, ATM, etc...) and wireless (10 cents, digital messaging, etc...) because of pro-competitive, open access policies in long-distance, data over dial-up, and wireless interconnect/roaming. If Roslyn Layton (pictured below) did not conveniently forget these facts or does not understand both the relative and absolute impacts on price and infrastructure investment then she would answer the following questions differently:

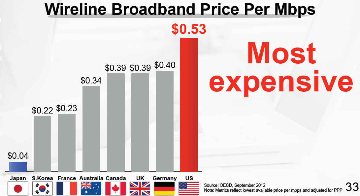

Real Reason/Answer: our bandwidth is 20-150x overpriced on a per bit basis because we disconnected from moore's and metcalfe's laws 10 years ago, due to the Telecom Act, then special access "de"regulation, then Brand-X or shutting down equal access for broadband. This rate differential is shown in the discrepancy between rates we pay in NYC and what Google charges in KC, as well as the difference in performance/price of 4G and wifi. It is great Roslyn can pay $3-5 a day for Starbucks. Most people can't (and shouldn't have to) just for a cup a Joe that you can make at home for 10-30 cents.

Real Reason/Answer: Because of their vertical business models, carriers are not well positioned to generate high ROI on rapidly depreciating technology and inefficient operating expense at every layer of the "stack" across geographically or market segment constrained demand. This is the real legacy of inefficient monopoly regulation. Doing away with regulation, or deregulating the vertical monopoly, doesn’t work. Both the policy and the business model need to be approached differently. Blueprints exist from the 80s-90s that can help us restructure our inefficient service providers. Basically, any carrier that is granted a public ROW (right of way) or frequency should be held to an open access standard in layer 1. The quid pro quo is that end-points/end-users should also have equal or unhindered access to that network within (economic and aesthetic) reason. This simple regulatory fix solves 80% of the problem as network investments scale very rapidly, become pervasive, and can be depreciated quickly.

Real Reason/Answer: Quasi monopolies exist in video for the cable companies and in coverage/standards in frequencies for the wireless companies. These scale economies derived from pre-existing monopolies or duopolies granted by and maintained to a great degree by the government. The only open or equal access we have left from the 1980s-90s (the drivers that got us here) is wifi (802.11) which is a shared and reusable medium with the lowest cost/bit of any technology on the planet as a result. But other generative and scalabeable standards developed in the US or with US companies at the same time, just like the internet protocol stacks, including mobile OSs, 4G LTE (based on CDMA/OFDM technology), OpenStack/Flow that now rule the world. It's very important to distinguish which of these are truly open or not.

Real Reason/Answer: The 3rd of the population who don't have/use broadband is as much because of context and usability, whether community/ethnicity, age or income levels, as cost and awareness. If we had balanced settlements in the middle layers based on transaction fees and pricing which reflect competitive marginal cost, we could have corporate and centralized buyers subsidizing the access and making it freely available everywhere for everyone. Putting aside the ineffective debate between bill and keep and 2-sided pricing models and instead implementing balanced settlement exchange models will solve the problem of universal HD tele-work, education, health, government, etc… We learned in the 1980s-90s from 800 and internet advertising that competition can lead to free, universal access to digital "economies". This is the other 20% solution to the regulatory problem.

Real Reason/Answer: The real issue here is that America led the digital information revolution prior to 1913 because it was a relatively open and competitive democracy, then took the world into 70 years of monopoly dark ages, finally breaking the shackles of monopoly in 1983, and then leading the modern information revolution through the 80s-90s. The US has now fallen behind in relative and absolute terms in the lower layers due to consolidation and remonopolization. Only the vestiges of pure competition from the 80s-90s, the horizontally scaled "data" and "content" companies like Apple, Google, Twitter and Netflix (and many, many more) are pulling us along. The vertical monopolies stifle innovation and the generative economic activity we saw in those 2 decades. The economic growth numbers and fiscal deficit do not lie.

I met the Godfather of New York Venture capital a few weeks ago and I was talking about an arbitrage opportunity of a lifetime in the communications sector. I started talking about the lack of competition and resulting high prices (which I highlighted last week) brought about by bandwidth being 20-150x overpriced. He just looked at me and said, “bandwidth issue? What bandwidth issue!” It just so happens that his current prize investment is an IPTV application. I just rolled my eyes thinking, “if he only knew!”, remembering what happened to all the web 1.0 companies that ran into the broadband brick wall in 2000.

This statement is symptomatic of the complacency amongst the venture community; those investing billions in the upper layers of the stack. Yet people on Main Street, as evidenced by the Kansas City Fiber video on the Fiber To The Home Council website indicating that 1,000 communities had responded to the contest with over 200,000 people directly involved, know otherwise.

The numbers tell a worse story. Because of the CLEC boom-bust 10-15 years ago, rescission of equal access, failure of muni-WiFi and Wimax and BTOP crowding-out Telecom spending has disconnected from other venture spending over the past decade. Based on overall VC spending telecom spending should be 2-3x greater than it is. Instead it stands 70% below where it was from 1995-2005. It took a while for competition to die, but now it is official!

Venture spending today for the sector, which used to average 15-20% of total VC spending is now down below 5% over the past 3 years. All the other TMT sectors have held nearly constant with overall VC spending.

Everyone should look at these numbers with alarm and reach out to policy makers, academics, trade folks, the venture community and capital markets to make them aware of the dearth of investment as a result of the lack of competition. Now, more than ever contrarian investors should look at the monopoly pricing and realize there is significant profits to be made at all layers of the stack.

67 million Americans live in rural areas. The FCC says the benchmark broadband speed is at least 4 Mbps downstream and 1 Mbps upstream. Based on that definition 65% of Americans actually have broadband, but only 50% who live in rural markets do; or 35 million. The 50% is due largely because 19 million Americans (28%) who live in rural markets do not even have access to these speeds. Another way of looking at the numbers shows that 97% of non-rural Americans have access to these speeds versus 72% living in rural areas. Rural Americans are at a significant disadvantage to other Americans when it comes to working from home, e-commerce or distance education. Clearly 70% are buying if they have access to it.

Furthermore we would argue the FCC standard is no longer acceptable when it comes to basic or high-definition multimedia, video and file downloads. These applications require 10+ Mbps downstream and 3+ Mbps upstream to make applications user friendly. Without those speeds you get what we call the "world-wide-wait" in rural markets for most of today's high-bandwidth applications. In the accompanying 2 figures we see a clear gap between the blue lines (urban) and green lines (rural) for both download and upload speeds. The result is that only 7% of rural Americans use broadband service with 6+/1.5+ Mbps versus 22% nationwide today.

The problem in rural markets is lack of alternative and affordable service providers. In fact the NTIA estimates that 4% of Americans have no broadband provider to begin with, 12% only 1 service provider and 44% just 2 providers. Almost all rural subscribers fall into 1 of these 3 categories. Rural utilities, municipalities, businesses and consumers would benefit dramatically from alternative access providers as economic growth is directly tied to broadband penetration.

The accompanying chart shows how vital broadband is to regional economic growth. If alternative access drives rural broadband adoption to levels similar to urban markets, then local economies will grow an additional 3% annually. That's because new wireless technology and applications such as home energy management, video on demand, video conferencing and distance learning provide the economic justification for alternative, lower-cost, higher bandwidth solutions.

Is the web dead?According to George Colony, CEO of Forrester, at LeWeb (Paris, Dec 7-9) it is; and on top of that social is running out of time, and social is where the enterprise is headed.A lot to digest at once, particularly when Google’s Schmidt makes a compelling case for a revolutionary smartphone future that is still in its very, very early stages; courtesy of an ice cream sandwich.

Ok, so let’s break all this down.The Web, dead?Yes Web 1.0 is officially dead, replaced by a mobile, app-driven future.Social is saturated?Yes, call it 1.0 and Social 2.0 will be utilitarian.Time is money, knowledge is power.Social is really knowledge and that’s where enterprises will take the real-time, always connected aspect of the smartphone ice cream sandwich applications that harness internal and external knowledge bases for rapid product development and customer support. Utilitarian.VIVA LA REVOLUTION!

Web 1.0 was a direct outgrowth of the breakup of AT&T; the US’ second revolution 30 years ago coinciding ironically with the bicentennial end of the 1st revolution.The bandwidth bottleneck of the 1960s and 1970s (the telephone monopoly tyranny) that gave rise to Microsoft and Intel processing at the edge vs the core, began to reverse course in the late 1980s and early 1990s as a result of flat-rate data access and an unlimited universe of things to easily look for (aka web 1.0). This flat-rate processing was a direct competitive response by the RBOCs to the competitive WAN (low-cost metered) threat.

As silicon scaled via Moore’s law (the WinTel sub-revolution) digital mobile became a low-cost, ubiquitous reality.The same pricing concepts that laid the foundation for web 1.0 took hold in the wireless markets in the US in the late 1990s; courtesy of the software defined, high-capacity CDMA competitive approach (see pages 34 and 36) developed in the US.

The US is the MOST important market in wireless today and THE reason for its leadership in applications and smart cloud.(Incidentally, it appears that most of LeWeb speakers were either American or from US companies.)In the process the relationship between storage, processing and network has come full circle (as best described by Ben Horowitz).The real question is, “will the network keep up?”Or are we doomed to repeat the cycle of promise and dashed hopes we witnessed between 1998-2003?

The answer is, “maybe”; maybe the communications oligopolies will liken themselves to IBM in front of the approaching WinTel tsunami in 1987.Will Verizon be that service provider that recognizes the importance of and embraces open-ness and horizontalization?The 700 mhz auctions and recent spectrum acquisitions and agreements with the major cable companies might be a sign that they do.

But a bigger question is whether Verizon will adopt what I call a "balanced payment (or settlement) system" and move away from IP/ethernet’s "bill and keep" approach.A balanced payment or settlement system for network interconnection simultaneously solves the issues of new service creation AND paves the way for the applications to directly drive and pay for network investment.So unlike web 1.0 where communication networks were resistently pulled into a broadband present, maybe they can actually make money directly off the applications; instead of the bulk of the value accruing to Apple and Google.

Think of this as an “800” future on steroids or super advertising, where the majority of access is paid for by centralized buyers.It’s a future where advertising, product marketing, technology, communications and corporate strategy converge.This is the essence of what Colony and Schmidt are talking about. Will Verizon CEO Seidenberg, or his rivals, recognize this? That would indeed be revolutionary!

Look up the definition of information and you’ll see a lot of terminology circularity.It’s all-encompassing and tough to define.It’s intangible, yet it drives everything we do.But information is pretty useless without people; in fact it doesn’t really exist.Think about the tree that fell, unseen, in the forest.Did it really fall?I am interested in the velocity of information, its impact on economies, societies, institutions and as a result in the development of communication networks and exchange of ideas.

Over the past several years I have increasingly looked at the relationship between electricity and communications.The former is the number one ingredient for the latter.Ask anybody in the data-center or server farm world.The relationship is circular.One wonders why the NTIA under its BTOP program didn’t figure that out; or at least talk to the DOE.Both spent billions separately, instead of jointly.Gee, why didn’t we add a 70 kV line when we trenched fiber down that remote valley?

Cars, in moving people (information) around, are a communications network, too; only powered by gasoline.Until now.The advent of electric vehicles (EV) is truly exciting.Perhaps more than the introduction of digital cell phones nearly 20 years ago.But to realize that future both the utility and auto industries should take a page from the competitive wireless playbook.

What got me thinking about all this was aNYT article this week about Dan Akerson, a former MCI CFOand Nextel CEO, who has been running (and shaking up) GM over the past 15 months.It dealt specifically with Dan’s handling of the Chevy Volt fires.Knowing Dan personally, I can say he is up to the task.He is applying lessons learned from the competitive communications markets to the competitive automotive industry.And he will win.

But will he and the automotive industry lose because of the utility industry?You see, the auto industry, the economy and the environment have a lot to gain from the development of electric vehicles (EV).Unfortunately the utility industry, which is 30 years behind the communications and IT revolution “digitizing” its business model, is not prepared for an EV eventuality.Ironically, utilities stand in the way of their own long-term success as EV’s would boost demand dramatically.

A lot has been spent on a “smart grid” with few meaningful results.Primarily this is because most of the efforts and decisions are being driven by insiders who do not want to change the status quo.The latter includes little knowledge of the consumer, a 1-way mentality, and a focus on average peak production and consumption.Utilities and their vendors loathe risk and consider real time to be 15 minutes going down to 5 minutes and view the production and consumption of electricity to be paramount.Smart-grid typically means the opposite, or a reduction in revenues.

So, it’s no surprise that they are building a smart-grid which does not give the consumer choice, flexibility and control, nor the ability to contribute to electricity production and be rewarded to be efficient and socially responsible.Nor do they want a lot of big-data to analyze and make the process even more efficient.Funny those are all byproducts of the competitive communications and IT industries we’ve become accustomed to.

So maybe once Dan has solved GM’s problems and recognizes the problems facing an electric vehicle future, he will focus his and those of his private equity brethren’s interests on developing a market-driven smart-grid; not one your grandmother’s utility would build.

By the way, here’s a “short”, and by no means exhaustive, list of alliances and organizations and the members involved in developing standards and approaches to the smart grid.Note: they are dominated by incumbents, and they all are comprised differently!

Be careful what you wish for this holiday season?After looking at Saks’ 5th Avenue “Snowflake & Bubbles” holiday window and sound and light display, I couldn’t help but think of a darker subtext.I had to ask the question answered infamously by Rolling Stone back in 2009, “who are the bubble makers?”The fact that this year’s theme was the grownup redux from last year’s child fantasy by focusing on the “makers” was also striking.An extensive google search reveals that NO ONE has tied either years’ bubble themes to manias in the broader economy or to the 1%.In fact, the New York Times called them “new symbols of joy and hope.”Only one article referenced the recession and hardship for many people as a stark backdrop for such a dramatic display.Ominously, one critic likened it to the “Nutcracker with bubbles” and we all know what happened to Tsarist Russia soon thereafter.

The light show created by Iris is spectacular and portends what I believe to be a big trend in the coming decade, namely using the smartphone to interact with signs and displays in the real world.It is not unimaginable that every device will soon have a wifi connection and be controllable via an app from a smartphone.Using the screen to type a message or draw an illustration that appears on a sign is already happening.CNBC showcased the windows as significant commercial and technical successes, which they were.Ironically the 1% appear to be doing just fine as Saks reported record sales in November.

Perhaps the lack of critical commentary has something to do with how quickly Occupy Wall Street rose and fell.Are we really living in a Twitter world?Fascinated and overwhelmed by trivia and endless information?At least the displays were sponsored by FIAT, who is trying to revive two brands in the US market simultaneously, focusing on the very real-world pursuit of car manufacturing.The same, unfortunately, cannot be said about MasterCard, (credit) bubble makers extraordinaire.Manias and speculative bubbles are not new and they will not go away.I’ve seen two build first hand and know that little could have been done to prevent them.So it will be in the future.

One was the crash in 1987 of what I like to call the “bull-sheet market of the 1980s”.More than anything, the 1980s was marked by the ascendance of the spreadsheet as a forecasting tool.Give a green kid out of business school a tool to easily extrapolate logarithmic growth and you’ve created the ultimate risk deferral process; at least until the music stops in the form of one down year in the trend.Who gave these tools out and blessed their use?The bubble makers (aka my bosses).But the market recovered and went to significant new highs (and speculative manias).

Similarly, a new communications paradigm (aka the internet) sprang to life in the early to mid 1990s as a relatively simply store and forward, database look-up solution.By the end of the 1990s there was nothing the internet could not do, especially if communications markets remained competitive.I remember the day in 1999 when Jeff Bezos said, in good bubble maker fashion, that “everyone would be buying goods from their cellphones” as a justification for Amazon’s then astronomical value of $30bn.I was (unfortunately) smart enough to know that scenario was a good 5-10 years in the future. 10 years later it was happening and AMZN recently exceeded $100bn, but not before dropping below $5bn in 2001 along with $5 trillion of wealth evaporating in the market.

If the spreadsheet and internet were the tools of the bubble makers in the 1980s and 1990s, then wireless was the primary tool of the bubble makers in the 2000s.Social media went into hyperdrive with texting, tweeting and 7x24 access from 3G phones apps. Arguably wireless mobility drove people's transiency and ability to move around aiding the housing bubble.So then what is the primary tool of the bubble makers in the 2010s?Arguably it is and will be the application ecosystems of iOS and Android.And what could make for an ugly bubble/burst cycle?Lack of bandwidth and lack of efficient clearinghouse systems (payments) for connecting networks.

But with a strong message to the markets in Washington DC on March 11 from

But with a strong message to the markets in Washington DC on March 11 from

education. Clearly 70% are buying if they have access to it.

education. Clearly 70% are buying if they have access to it. both download and upload speeds. The result is that only 7% of rural Americans use broadband service with 6+/1.5+ Mbps versus 22% nationwide today.

both download and upload speeds. The result is that only 7% of rural Americans use broadband service with 6+/1.5+ Mbps versus 22% nationwide today. The accompanying chart shows how vital broadband is to regional economic growth. If alternative access drives rural broadband adoption to levels similar to urban markets, then local economies will grow an additional 3% annually. That's because new wireless technology and applications such as home energy management, video on demand, video conferencing and distance learning provide the economic justification for alternative, lower-cost, higher bandwidth solutions.

The accompanying chart shows how vital broadband is to regional economic growth. If alternative access drives rural broadband adoption to levels similar to urban markets, then local economies will grow an additional 3% annually. That's because new wireless technology and applications such as home energy management, video on demand, video conferencing and distance learning provide the economic justification for alternative, lower-cost, higher bandwidth solutions.