The US has lacked a telecom network visionary for nearly 2 decades. There have certainly been strong and capable leaders, such as John Malone who not only predicted but brought about the 500 channel LinearTV model. But there hasn’t been someone like Bill McGowan who broke up AT&T or Craig McCaw who first had the vision to build a national, seamless wireless network, countering decades of provincial, balkanized thinking. Both of them fundamentally changed the thinking around public service provider networks.

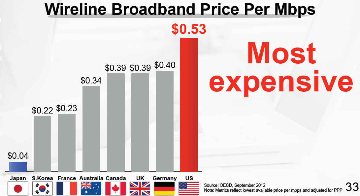

But with a strong message to the markets in Washington DC on March 11 from Masayoshi Son, Sprint’s Chairman, the 20 year wait may finally be over. Son did what few have been capable of doing over the past 15-20 years since McGowan exited stage left and McCaw sold out to MaBell: telling it like it is. The fact is that today’s bandwidth prices are 20-150x higher than they should be with current technology.

This is no one’s fault in particular and in fact to most people (even informed ones) all measures of performance-to-price compared to 10 or 20 years ago look great. But, as Son illustrated, things could be much, much better. And he’s willing to make a bet on getting the US, the most advanced and heterogeneous society, back to a leadership role with respect to the ubiquity and cost of bandwidth. To get there he needs more scale and one avenue is to merge with T-Mobile.

There have been a lot of naysayers as to the possibility of a Sprint-T-Mo hookup, including leaders at the FCC. But don’t count me as one; it needs to happen. Initially skeptical when the rumors first surfaced in December, I quickly reasoned that a merger would be the best outcome for the incentive auctions. A merger would eliminate spectrum caps as a deterrent to active bidding and maximize total proceeds. It would also have a better chance of developing a credible third competitor with equal geographic reach. Then in January the FCC and DoJ came out in opposition to the merger.

In February, though, Comcast announced the much rumored merger with TW and Son jumped on the opportunity to take his case for merging to a broader stage. He did so in front of a packed room of 300 communications pundits, press and politicos at the US Chamber of Commerce’s prestigious Hall of Flags; a poignant backdrop for his own rags to riches story. Son’s frank honesty about the state of broadband for the American public vs the rest of the world, as well as Sprint’s own miserable current performance were impressive. It’s a story that resonates with my America’s Bandwidth Deficit presentation.

Here are some reasons the merger will likely pass:

The FCC can’t approve one horizontal merger (Comcast/TW) that brings much greater media concentration and control over content distribution, while disallowing a merger of two small players (really irritants as far as AT&T and Verizon are concerned).

Son has a solid track record of disruption and doing what he says.

The technology and economics are in his favor.

The vertically integrated service provider model will get disrupted faster and sooner as Sprint will have to think outside the box, partner, and develop ecosystems that few in the telecom industry have thought about before; or if they have, they’ve been constrained by institutional inertia and hidebound by legacy regulatory and industry siloes.

Here are some reasons why it might not go through:

The system is fundamentally corrupt. But the new FCC Chairman is cast from a different mold than his predecessors and is looking to make his mark on history.

The FCC shoots itself in the foot over the auctions. Given all the issues and sensitivities around incentive auctions the FCC wants this first one to succeed as it will serve as a model for all future spectrum refarming issues.

The FCC and/or DoJ find in the public interest that the merger reduces competition. But any analyst can see that T-Mo and Sprint do not have sustainable models at present on their own; especially when all the talk recently in Barcelona was already about 5G.

Personally I want Son’s vision to succeed because it’s the vision I had in 1997 when I originally brought the 2.5-2.6 (MMDS) spectrum to Sprint and later in 2001 and 2005 when I introduced Telcordia’s 8x8 MIMO solutions to their engineers. Unfortunately, past management regimes at Sprint were incapable of understanding the strategies and future vision that went along with those investment and technology pitches. Son has a different perspective (see in particular minute 10 of this interview with Walt Mossberg) with his enormous range of investments and clear understanding of price elasticity and the marginal cost of minutes and bits.

To be successful Sprint’s strategy will need to be focused, but at the same time open and sharing in order to simultaneously scale solutions across the three major layers of the informational stack (aka the InfoStack):

upper (application and content)

middle (control)

lower (access and transport)

This is the challenge for any company that attempts to disrupt the vertically integrated telecom or LinearTV markets; the antiquated and overpriced ones Son says he is going after in his presentation. But the US market is much larger and more robust than the rest of the world, not just geographically, but also from a 360 degree competitive perspective where supply and demand are constantly changing and shifting.

Ultimate success may well rest in the control layer, where Apple and Google have already built up formidable operating systems which control vastly profitably settlement systems across multiple networks. What few realize is that the current IP stack does not provide price signals and settlement systems that clear supply and demand between upper and lower layers (north-south) or between networks (east-west) in the newly converged “informational” stack of 1 and 2-way content and communications.

If Sprint’s Chairman realizes this and succeeds in disrupting those two markets with his strategy then he certainly will be seen as a visionary on par with McGowan and McCaw.

Is IP Growing UP? Is TCPOSIP the New Protocol Stack? Will Sessions Pay For Networks?

Oracle’s purchase of leading SBC vendor (session border controller Acme Packets), is a tiny seismic event in the technology and communications (ICT) landscape. Few notice the potential for much broader upheaval ahead.

SBCs, which have been around since 2000, facilitate traffic flow between different networks; IP to PSTN to IP and IP to IP. Historically traffic has been mostly voice, where minutes and costs count because that world has been mostly rate-based. Increasingly they are being used to manage and facilitate any type of traffic “sessions” across an array of public and private networks, be it voice, data, or video. The reasons are many-fold, including, security, quality of service, cost, and new service creation; all things TCP-IP don't account for.

Session control is layer 5 to TCP-IP’s 4 layer stack. A couple of weeks ago I pointed out that most internet wonks and bigots deride the OSI framework and feel that the 4 layer TCP-IP protocol stack won the “war”. But here is proof that as with all wars the victors typically subsume the best elements and qualities of the vanquished.

The single biggest hole in the internet and IP world view is bill and keep. Bill and keep’s origins derive from the fact that most of the overhead in data networks was fixed in the 1970s and 1980s. The component costs were relatively cheap compared with the mainframe costs that were being shared and the recurring transport/network costs were being arbitraged and shared by those protocols. All the players, or nodes, were known and users connected via their mainframes. The PC and ethernet (a private networking/transmission protocol) came along and scaled much later. So why bother with expensive and unnecessary QoS, billing, mediation and security in layers 5 and 6?

Then along came the break-up of AT&T and due to dial-1 equal access, the Baby Bells responded with flat-rate, expanded area (LATA) pricing plans to build a bigger moat around their Class 5 monopoly castles (just like AT&T had built 50 mile interconnect exclusion zones in the 1913 Kingsbury Commitment due to the threat of wireless bypass even back then, and just like the battles OTT providers like Netflix are having with incumbent broadband monopolies today) in the mid to late 1980s. The nascent commercial ISPs took advantage of these flat-rate zones, invested in channel banks, got local DIDs and the rest as they say is history. Staying connected all day on a single flat-rate back then was perceived of as "free". So the "internet" scaled from this pricing loophole (even as the ISPs received much needed shelter from vertical integration by the monopoly Bells in Computers 2/3) and further benefited from WAN competition and commoditization of transport to connect all the distributed router networks into seamless regional and national layer 1-2 low-cost footprints even before www and http/html and the browser hit in the early to mid 1990s. The marginal cost of "interconnecting" these layer 1-2 networks was infinitesimal at best and therefore bill and keep, or settlement-free peering, made a lot of sense.

But Bill and Keep (B&K) has three problems:

It supports incumbents and precludes new entrants

It stifles new service creation

It precludes centralized procurement and subsidization

With Acme, Oracle can provide solutions to problems two and three; with the smartphone driving the process. Oracle has java on 3 billion phones around the globe. Now imagine a session controller client on each device that can help with application and access management and preferential routing and billing etc, along with guaranteed QoS and real-time performance metrics and auditing; regardless of what network the device is currently on. The same holds in reverse in terms of managing "session state" across multiple devices/screens across wired and wireless networks.

The alternative to B&K is what I refer to as balanced settlements. In traditional telecom parlance, instead of just being calling party pays, they can be both called and calling party pays and are far from the regulated monopoly origination/termination tariffs. Their pricing (transaction fees) will reflect marginal costs and therefore stimulate and serve marginal demand. As a result, balanced settlements provide a way for rapid, coordinated roleout of new services and infrastructure investment across all layers and boundary points. They provide the price signals that IP does not.

Balanced settlements clear supply and demand north-south between upper (application) and lower (switching,transport and access) layers, as well as east-west from one network or application or service provider to another. Major technological shifts in the network layers like open flow, software defined networks (SDN) and network function virtualization (NFV) can develop rapidly. Balanced settlements will reside in competitive exchanges evolving out of today's telecom tandem networks, confederation of service provider APIs, and the IP world's peering fabric, driven by big data analytical engines and advertising exchanges.

Perhaps most importantly, balanced settlements enable subsidization or procurement of edge access from the core. Large companies and institutions can centrally drive and pay for high definition telework, telemedicine, tele-education, etc... solutions across a variety of access networks (fixed and wireless). The telcos refer to this as guaranteed quality of service leading to "internet fast lanes." Enterprises will do this to further digitize and economize their own operations and distribution reach (HD collaboration and the internet of things), just like 800, prepaid calling cards, VPNs and the internet itself did in the 1980s-90s. I call this process marrying the communications event to the commercial/economic transaction and it results in more revenue per line or subscriber than today's edge subscription model. As well, as more companies and institutions increasingly rely on the networks, they will demand backups, insurance and redundancy ensuring that there will be continous investment in multiple layer 1 access networks.

Along with open or shared access in layer 1 (something we should have agreed to in principal back in 1913 and again in 1934 as governments provide service providers a public right of way or frequency), balanced settlements can also be an answer to inefficient universal service subsidies. Three trends will drive this. Efficient loading of networks and demand for ubiquitous high-definition services by mobile users will require inexpensive uniform access everywhere with concurrent investment in high-capacity fiber and wireless end-points. Urban demand will naturally pay for rural demand in the process due to societal mobilty and finally the high volume low marginal cost user (enterprise or institution) will amortize and pay for the low-volume high marginal cost user to be part of their "economic ecosystem" thereby reducing the digital divide.

Is reality mimicking art?Is Android following the script from Genesis’ epochal hit Land of Confusion? Is it a bad dream on this day that happens once every four years?Yes, yes, and unfortunately no.Before I go into a litany of ills besetting the Android market and keeping Apple shareholders very happy, two points: a) I have an HTC Incredible and am a Droid fan, and b) the 1986 hit parodied superpower conflict and inept decisions by global leaders but presaged the fall of the Berlin Wall and 20+ years of incredible growth, albeit with a good deal of 3rd world upheaval in the Balkans, Mid-east, and Africa.So maybe there is hope that out of the current state a new world order will arise as the old monopolies are dismantled.

Apple clearly has the digital formula right at present; simplicity, ease of use, performance, and yet, at the same time unlimited choice and customization.Contrast that with this parody from SNL of Verizon and 4G/3G/2G/noG and the Samsung Superbowl Ad portraying a wild party.The result is a disturbing trend if you are an Android phone lover. The ecosystem’s rate of new technology adoption is slowing down even if better technology is being made as consumers are clearly confused. In the tablet market there is even a greater disparity, with Android tablets hardly making a dent in Apple's share.

Yesterday Eric Schmidt prognosticated at MWC a world where more is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.Yet, at the same time Apple managed to steal the show with its iPad3 announcement.Contrast this with HTC rolling out some awesome phones that will not be available in the US this year because their chip doesn't support 4G.

The answer is not better technology, but better ecosystems.The Droid device vendors should realize this and build a layer of software and standards above Google/ICS to facilitate interoperability across silos (at the individual, device and network level); instead of just depreciating their hardware value by competing on price and features many people do not want. They can then collectively win in residual transaction streams (like collectively synching back to a dropbox) like Apple.

Examples of these include standardization and interoperability of free or subsidized wifi offload, over the top messaging, voice and other solutions and the holy grail, mobile payments. Companies like CloudFoundry allows for cross Cloud application infrastructure support, with AppFog and Iron Foundry are pursuing these approaches individually. But just think what would happen if Samsung, HTC, LG and Motorola were to band together and coordinate these approaches and develop very low cost balanced payment systems within the Droid ecosystem to promote interoperability and cooperation, counteract Google and restore some sanity to the market. Carriers (um battleships?) will not be able to stop this effort and may even welcome it just as the music industry opened its arms to Apple.

Apple hasn’t been an innovator so much as a great design company that understands big market opportunities and what the customer wants. The result is an established order that other industries and their customers clearly prefer. Millenials are too young to know Land of Confusion, but the current decision makers in the Droid ecosystem do and so they should take a lesson from history on this Leap Day.Hopefully we’ll wake up in 4 years and there will be a wonderful new world order. Oh, and a Happy 4 Birthdays to everyone present and past who was born on this day.

Wireless service providers (WSPs) like AT&T and Verizon are battleships, not carriers.Indefatigable...and steaming their way to disaster even as the nature of combat around them changes.If over the top (OTT) missiles from voice and messaging application providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then Dropbox bombs are about to score direct hits near their water lines.The WSPs may well sink from new combatants coming out of nowhere with excellent synching and other novel end-user enablement solutions even as pundits like Tomi Ahonen and others trumpet their glorious future.Full steam ahead.

Instead, WSP captains should shout “all engines stop” and rethink their vertical integration strategies to save their ships.A good start might be to look where smart VC money is focusing and figure out how they are outfitted at each level to defend against or incorporate offensively these rapidly developing new weapons.More broadly WSPs should revisit the WinTel wars, which are eerily identical to the smartphone ecosystem battles, and see what steps IBM took to save its sinking ship in the early 1990s.One unfortunate condition might be that the fleet of battleships are now so widely disconnected that none have a chance to survive.

The bulls on Dropbox (see the pros and cons behind the story) suggest that increased reliance on cloud storage and synching will diminish reliance on any one device, operating system or network.This is the type of horizontalization we believe will continue to scale and undermine the (perceived) strength of vertical integration at every layer (upper, middle and lower).Extending the sea battle analogy, horizontalization broadens the theatre of opportunity and threat away from the ship itself; exactly what aircraft carriers did for naval warfare.

Synching will allow everyone to manage and tailor their “states”, developing greater demand opportunity; something I pointed out a couple of months ago.People’s states could be defined a couple of ways, beginning with work, family, leisure/social across time and distance and extending to specific communities of (economic) interest.I first started talking about the “value of state” as Chief Strategist at Multex just as it was being sold to Reuters.

Back then I defined state as information (open applications, communication threads, etc...) resident on a decision maker’s desktop at any point in time that could be retrieved later.Say I have multiple industries that I cover and I am researching biotech in the morning and make a call to someone with a question.Hours later, after lunch meetings, I am working on chemicals when I get a call back with the answer.What’s the value of bringing me back automatically to the prior biotech state so I can better and more immediately incorporate and act on the answer?Quite large.

Fast forward nearly 10 years and people are connected 7x24 and checking their wireless devices on average 150x/day.How many different states are they in during the day?5, 10, 15, 20?The application world is just beginning to figure this out.Google, Facebook, Pinterest and others are developing data engines that facilitate “free access” to content and information paid for by centralized procurement; aka advertising.Synching across “states” will provide even greater opportunity to tailor messages and products to consumers.

Inevitably those producers (advertisers) will begin to require guaranteed QoS and availability levels to ensure a good consumer experience. Moreover, because of social media and BYOD companies today are looking at their employees the same way they are looking at their consumers.The overall battlefield begins to resemble the 800 and VPN wars of the 1990s when we had a vibrant competitive service provider market before its death at the hands of the 1996 Telecom Act (read this critique and another that questions the Bell's unnatural monopoly).Selling open, low-cost, widely available connectivity bandwidth into this advertising battlefield can give WSPs profit on every transaction/bullet/bit across their network.That is the new “ship of state” and taking the battle elsewhere.Some call this dumb pipes; I call this a smart strategy to survive being sunk.

A humble networking protocol 10 years ago, packet based Ethernet (invented at Xerox in 1973) has now ascended to the top of the carrier networking pyramid over traditional voice circuit (time) protocols due to the growth in data networks (storage and application connectivity) and 3G wireless.According to AboveNet the top 3 CIO priorities are cloud computing, virtualization and mobile, up from spots 16, 3 and 12, respectively, just 2 years ago! Ethernet now accounts for 36% of all access, larger than any other single legacy technology, up from nothing 10 years ago when the Metro Ethernet Forum was established.With Gigabit and Terabit speeds, Ethernet is the only protocol for the future.

The recent Ethernet Expo 2011 in NYC underscored the trends and importance of what is going on in the market.Just like fiber and high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2).This graphic illustrates why it has spread through the landscape so rapidly from LAN to MAN to WAN.With 75% of US business buildings lacking access to fiber, EoC will be the preferred access solution.As bandwidth demand increases, Ethernet has a 5-10x price/performance advantage over legacy equipment.

Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology).The graphic below shows how the growing horizontalization is supported by vertical integration of information (ie exchanges) that will make Ethernet truly “on-demand”.This model is critical because of both the variability and dispersion of traffic brought on by both mobility and cloud computing.Already, the underlying layers are being “re”-developed by companies like AlliedFiber who are building new WAN fiber with interconnection points every 60 miles.It will all be ethernet.Ultimately, app providers may centralize intelligence at these points, just like Akamai pushed content storage towards the edge of the network for Web 1.0.At the core and key boundary points Ethernet Exchanges will begin to develop.Right now network connections are mostly private and there is significant debate as to whether there will be carrier exchanges.The reality is that there will be exchanges in the future; and not just horizontal but vertical as well to facilitate new service creation and a far larger range of on-demand bandwidth solutions.

By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.It is consistent with my own definition of web 1.0 as a 4 layer stack.Replace layer 4 with clouds and mobile and you get the sense for how much greater complexity there is today.When you compare it to the above charts you see how far Ethernet has evolved in a very rapid time and why companies like Telx, Equinix (8.6x cash flow), Neutral Tandem (3.5x cash flow) will be interesting to watch, as well as larger carriers like Megapath and AboveNet (8.2x cash flow).Certainly the next 3-5 years will see significant growth in ethernet and obsolescence of the PSTN and legacy voice (time-based) technologies.

But with a strong message to the markets in Washington DC on March 11 from

But with a strong message to the markets in Washington DC on March 11 from

and unfortunately no.

and unfortunately no. Apple clearly has the

Apple clearly has the  is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.

is better and cheaper; which may be good for Google but not necessarily the best thing for anyone else in the Droid ecosystem, including consumers.

providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then

providers started fires on their superstructures and WiFi offload torpedoes from alternative carriers and enterprises opened cracks in their hulls, then  d high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2).

d high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2). Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology).

Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology). By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.

By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.