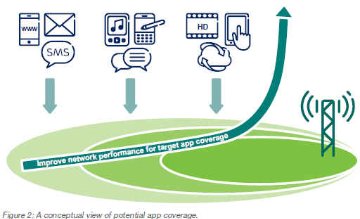

Given the smartphone’s ubiquity and our dependence on it, “App Coverage” (AC) is something confronting us every day, yet we know little about it. At the CCA Global Expo this week in San Antonio Glenn Laxdal of Ericsson spoke about “app coverage”, which the vendor first surfaced in 2013. AC is defined as, “the proportion of a network’s coverage that has sufficient performance to run a particular app at an acceptable quality level.” In other words the variety of demand from end-users for voice, data and video applications is outpacing the ability of carriers to keep up. According to Ericsson, monitoring and ensuring performance of app coverage is the next wave in LTE networks. Here’s a good video explaining AC in simple, visual terms.

Years, nay, decades ago I used to say coverage should be measured in 3 important ways:

Geographic (national vs regional vs local)

In/Outdoors (50+% loss indoors)

Frequency (double capex 1900 vs 700 mhz)

Each of these had specific supply/demand clearing implications across dozens of issues impacting balance sheets and P&L statements; ultimately determining winners and losers. They are principally why AT&T and Verizon today have 70% of subscribers (80% of enterprise customers) up from 55% just 5 years ago, 84% of total profit, and over 100% of industry free cash flow. Now we can add “applications” to that list. And it will only make it more challenging for competitors to wrestle share from the “duopoly”.

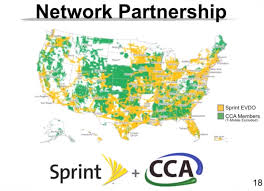

Cassidy Shield of Alcatel-Lucent, further stated that fast follower strategies to the duopoly would likely fail; implying that radical rethinking was necessary. Some of that came quickly in the form of Masayoshi Son’s announcement of a broad partnership with NetAmerica and members of CCA for preferred roaming, concerted network buildout and sharing of facilities and device purchase agreements. This announcement came two weeks after Son visited Washington DC and laid out Sprint’s vision for a new, more competitive wireless future in America.

The conference concluded with a panel of CEOs hailing Sprint’s approach, which Son outlined here, as one of benevolent dictator (perhaps not the best choice of words) and exhorting the label partner, partner, partner; something that Terry Addington of MobileNation has said has taken way too long. Even then the panel agreed that pulling off partnerships will be challenging.

The Good & Bad of Wireless

Wireless is great because it is all things to all people, and that is what makes it bad too. Planning for and accounting how users will access the network is very challenging across a wide user base. There are fundamentally different “zones” and contexts in which different apps can be used and they often conflict with network capacity and performance. I used to say that one could walk and also hang upside down from a tree and talk, but you couldn’t “process data” doing those things. Of course the smartphone changed all that and people are accessing their music apps, location services, searches, purchases, and watching video from anywhere; even hanging upside down in trees.

Today voice, music and video consume 12, 160 and 760 kpbs of bandwidth, respectively, on average. Tomorrow those numbers might be 40, 500, 1500, and that’s not even taking into account “upstream” bandwidth which will be even more of a challenge for service providers to provision when consumers expect more 2-way collaboration everywhere. The law of wireless gravity, which states bits will seek out fiber/wire as quickly and cheaply as possible, will apply, necessitating sharing of facilities (wireless and wired), heterogeneous network (Hetnet), and aggressive wifi offload approaches; even consumers will be shared in the form of managed services across communities of users (known today as OTT). The show agenda included numerous presentations on distributed antennae networks and wifi offload applied to the rural coverage challenge.

Developing approaches ex ante to anticipate demand is even more critical if carriers want to play major roles in the internet of things, unified (video) communications and the connected car. As Ericsson states in its whitepaper,

“App coverage integrates all aspects of network performance – including radionetwork throughput and latency, capacity, as well as the performance of the backhaul, packetcore and the content-delivery networks. Ultimately, managing app coverage and performance demands a true end-to-end approach to designing, building and running mobile networks.”

The US has lacked a telecom network visionary for nearly 2 decades. There have certainly been strong and capable leaders, such as John Malone who not only predicted but brought about the 500 channel LinearTV model. But there hasn’t been someone like Bill McGowan who broke up AT&T or Craig McCaw who first had the vision to build a national, seamless wireless network, countering decades of provincial, balkanized thinking. Both of them fundamentally changed the thinking around public service provider networks.

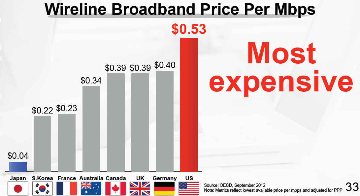

But with a strong message to the markets in Washington DC on March 11 from Masayoshi Son, Sprint’s Chairman, the 20 year wait may finally be over. Son did what few have been capable of doing over the past 15-20 years since McGowan exited stage left and McCaw sold out to MaBell: telling it like it is. The fact is that today’s bandwidth prices are 20-150x higher than they should be with current technology.

This is no one’s fault in particular and in fact to most people (even informed ones) all measures of performance-to-price compared to 10 or 20 years ago look great. But, as Son illustrated, things could be much, much better. And he’s willing to make a bet on getting the US, the most advanced and heterogeneous society, back to a leadership role with respect to the ubiquity and cost of bandwidth. To get there he needs more scale and one avenue is to merge with T-Mobile.

There have been a lot of naysayers as to the possibility of a Sprint-T-Mo hookup, including leaders at the FCC. But don’t count me as one; it needs to happen. Initially skeptical when the rumors first surfaced in December, I quickly reasoned that a merger would be the best outcome for the incentive auctions. A merger would eliminate spectrum caps as a deterrent to active bidding and maximize total proceeds. It would also have a better chance of developing a credible third competitor with equal geographic reach. Then in January the FCC and DoJ came out in opposition to the merger.

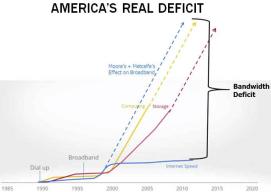

In February, though, Comcast announced the much rumored merger with TW and Son jumped on the opportunity to take his case for merging to a broader stage. He did so in front of a packed room of 300 communications pundits, press and politicos at the US Chamber of Commerce’s prestigious Hall of Flags; a poignant backdrop for his own rags to riches story. Son’s frank honesty about the state of broadband for the American public vs the rest of the world, as well as Sprint’s own miserable current performance were impressive. It’s a story that resonates with my America’s Bandwidth Deficit presentation.

Here are some reasons the merger will likely pass:

The FCC can’t approve one horizontal merger (Comcast/TW) that brings much greater media concentration and control over content distribution, while disallowing a merger of two small players (really irritants as far as AT&T and Verizon are concerned).

Son has a solid track record of disruption and doing what he says.

The technology and economics are in his favor.

The vertically integrated service provider model will get disrupted faster and sooner as Sprint will have to think outside the box, partner, and develop ecosystems that few in the telecom industry have thought about before; or if they have, they’ve been constrained by institutional inertia and hidebound by legacy regulatory and industry siloes.

Here are some reasons why it might not go through:

The system is fundamentally corrupt. But the new FCC Chairman is cast from a different mold than his predecessors and is looking to make his mark on history.

The FCC shoots itself in the foot over the auctions. Given all the issues and sensitivities around incentive auctions the FCC wants this first one to succeed as it will serve as a model for all future spectrum refarming issues.

The FCC and/or DoJ find in the public interest that the merger reduces competition. But any analyst can see that T-Mo and Sprint do not have sustainable models at present on their own; especially when all the talk recently in Barcelona was already about 5G.

Personally I want Son’s vision to succeed because it’s the vision I had in 1997 when I originally brought the 2.5-2.6 (MMDS) spectrum to Sprint and later in 2001 and 2005 when I introduced Telcordia’s 8x8 MIMO solutions to their engineers. Unfortunately, past management regimes at Sprint were incapable of understanding the strategies and future vision that went along with those investment and technology pitches. Son has a different perspective (see in particular minute 10 of this interview with Walt Mossberg) with his enormous range of investments and clear understanding of price elasticity and the marginal cost of minutes and bits.

To be successful Sprint’s strategy will need to be focused, but at the same time open and sharing in order to simultaneously scale solutions across the three major layers of the informational stack (aka the InfoStack):

upper (application and content)

middle (control)

lower (access and transport)

This is the challenge for any company that attempts to disrupt the vertically integrated telecom or LinearTV markets; the antiquated and overpriced ones Son says he is going after in his presentation. But the US market is much larger and more robust than the rest of the world, not just geographically, but also from a 360 degree competitive perspective where supply and demand are constantly changing and shifting.

Ultimate success may well rest in the control layer, where Apple and Google have already built up formidable operating systems which control vastly profitably settlement systems across multiple networks. What few realize is that the current IP stack does not provide price signals and settlement systems that clear supply and demand between upper and lower layers (north-south) or between networks (east-west) in the newly converged “informational” stack of 1 and 2-way content and communications.

If Sprint’s Chairman realizes this and succeeds in disrupting those two markets with his strategy then he certainly will be seen as a visionary on par with McGowan and McCaw.

How To Develop A Blue Ocean Strategy In A Digital Ecosystem

Back in 2002 I developed a 3 dimensional macro/micro framework based strategy for Multex, one of the earliest and leading online providers of financial information services. The result was to sell themselves to Reuters in a transaction that benefited both companies. 1+8 indeed equaled 12. What I proposed to the CEO was simple. Do “this” to grow to a $500m company or sell yourself. After 3-4 weeks of mulling it over, he took a plane to London and sold his company rather than undertake the “this”.

What I didn’t know at the time was that the “this” was a Blue Ocean Strategy (BOS) of creating new demand by connecting previously unconnected qualitative and quantitative information sets around the “state” of user. For example a portfolio manager might be focused on biotech stocks in the morning and make outbound calls to analysts to answer certain questions. Then the PM goes to a chemicals lunch and returns to focus on industrial products in the afternoon, at which point one of the biotech analysts gets back to him. Problem. The PM’s mental and physical “state” or context is gone. Multex had the ability to build a tool that could bring the PM back to his morning “state” in his electronic workplace. Result, faster and better decisions. Greater productivity, possible performance, definite value.

Sounds like a great story, except there was no BOS in 2002. It was invented in 2005. But the second slide of my 60 slide strategy deck to the CEO had this quote from the author’s of BOS, W.Chan Kim and Renee Mauborgne, of INSEAD, the Harvard Business School of Europe:

“Strategic planning based on drawing a picture…produces strategies that instantly illustrate if they will: stand out in the marketplace, are easy to understand and communicate, and ensure that every employee shares a single visual reference point.”

So you could argue that I anticipated the BOS concept to justify my use of 3D frameworks which were meant to illustrate this entirely new playing field for Multex.

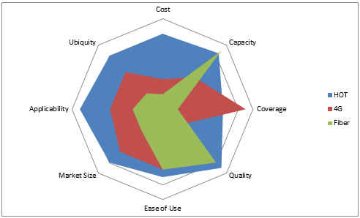

But this piece is less about the InfoStack’s use in business and sports and more about the use of the 4Cs and 4Us of supply and demand as tools within the frameworks to navigate rapidly changing and evolving ecosystems. And we use the BOS graphs postulated by Kim/Mauborgne. The 4Cs and 4Us lets someone introducing a new product, horizontal layer (exchange) or vertical market solution (service integration) figure out optimal product, marketing and pricing strategies and tactics a priori. A good example of this is a BOS I created for a project I am working on in the area of Wifi offload and Hetnet (heterogeneous access networks that can be self-organising) area called HotTowns (HOT). Here’s a picture of it comparing 8 key supply and demand elements across fiber, 4G macro cellular and super saturation offload in a rural community. Note that the "blue area" representing the results of the model can be enhanced on the capacity front by fiber and on the coverage front by 4G.

The same approach can be used to rate mobile operating systems and any other product at a boundary of the infostack or horizontal or vertical solution in the market. We'll do some of that in upcoming pieces.

Since I began covering the sector in 1990, I’ve been waiting for Big Bang II.An adult flick?No, the sequel to Big Bang (aka the breakup of MaBell and the introduction of equal access) was supposed to be the breakup of the local monopoly.Well thanks to the Telecom Act of 1996 and the well-intentioned farce that it was, that didn’t happen and equal access officially died (equal access RIP) in 2005 with the Supreme Court's Brand-X decision vs the FCC. If it died, then we saw a resurrection that few noticed.

I am announcing that Equal Access is alive and well, albeit in a totally unexpected way.Thanks to Steve Jobs’ epochal demands put on AT&T to counter its terrible 2/3G network coverage and throughput, every smartphone has an 802.11 (WiFi) backdoor built-in.Together with the Apple and Google operating systems being firmly out of carriers’ hands and scaling across other devices (tablets, etc…) a large ecosystem of over-the-top (OTT), unified communications and traffic offloading applications is developing to attack the wireless hegemony.

First, a little history. Around the time of AT&T's breakup the government implemented 2 forms of equal access. Dial-1 in long-distance made marketing and application driven voice resellers out of the long-distance competitors. The FCC also mandated A/B cellular interconnect to ensure nationwide buildout of both cellular networks. This was extended to nascent PCS providers in the early to mid 1990s leading to dramatic price declines and enormous demand elasticities. Earlier, the competitive WAN/IXC markets of the 1980s led to rapid price reductions and to monopoly (Baby Bell or ILEC) pricing responses that created the economic foundations of the internet in layers 1 and 2; aka flat-rate or "unlimited" local dial-up. The FCC protected the nascent ISP's by preventing the Bells from interfering at layer 2 or above. Of course this distinction of MAN/LAN "net-neutrality" went away with the advent of broadband, and today it is really just about WAN/MAN fights between the new (converged) ISPs or broadband service providers like Comcast, Verizon, etc... and the OTT or content providers like Google, Facebook, Netflix, etc...

(Incidentally, the FCC ironically refers to edge access providers, who have subsumed the term ISPs or "internet service providers", as "core" providers, while the over-the-top (OTT) messaging, communications, e-commerce and video streaming providers, who reside at the real core or WAN, are referred to as "edge" providers. There are way, way too many inconsistencies for truly intelligent people to a) come up with and b) continue to promulgate!)

But a third form of equal access, this one totally unintentioned, happened with 802.11 (WiFi) in the mid 1990s. The latter became "nano-cellular" in that power output was regulated limiting hot-spot or cell-size to ~300 feet. This had the impact of making the frequency band nearly infinitely divisible. The combination was electric and the market, unencumbered by monopoly standards and scaling along with related horizontal layer 2 data technologies (ethernet), quickly seeded itself. It really took off when Intel built WiFi capability directly into it's Centrino chips in the early 2000s. Before then computers could only access WiFi with usb dongles or cables tethered to 2G phones

Cisco just forecast that 50% of all internet traffic will be generated from 802.11 (WiFi) connected devices.Given that 802.11’s costs are 1/10th those of 4G something HAS to give for the communications carrier.We’ve talked about them needing to address the pricing paradox of voice and data better, as well as the potential for real obviation at the hands of the application and control layer worlds.While they might think they have a near monopoly on the lower layers, Steve Job’s ghost may well come back to haunt them if alternative access networks/topologies get developed that take advantage of this equal access. For these networks to happen they will need to think digital, understand, project and foster vertically complete systems and be able to turn the "lightswitch on" for their addressable markets.

I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice. John McQuillan and his Next Gen Networks (NGN) conferences were my inspiration and source. In the mid-2000s I used them to illustrate the potential for a world of unlimited demand ecosystems: commercial, consumer, social, financial, etc…Cloud computing has now become a part of everyday vernacular.The problem is that for cloud computing to expand the world of networks needs to go flat, or horizontal, as in this complex looking illustration to the left.

This is a static view.Add some temporality and rapidly shifting supply/demand dynamics and the debate begins as to whether the system should be centralized or decentralized.Yes and no.There are 3 main network types:hierarchical, centralized and fully distributed (aka peer to peer).None fully accommodate metcalfe’s, moore’s and zipf’s laws.Network theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many.Processing/intelligence initially must be centralized but then traffic and signaling volumes dictate pushing the intelligence to the edge. The illustration to the right begins to convey that lateral motion in a flat, layered architecture, driven by the 2-way, synchronous nature of traffic; albeit with the signalling and transactions moving vertically up and down.

But just as solutions begin to scale, a new service is borne superseding the original.This chaotic view from the outside looks like an organism in constant state of expansion then collapse, expansion then collapse, etc…

A new network theory that controls and accounts for this constant state of creative destruction* is Centralized Hierarchical Networks (CHNs) CC.A search on google and duckduckgo reveals no known prior attribution, so Information Velocity Partners, LLC (aka IVP Capital, LLC) both lays claim and offers up the term under creative commons (CC).I actually coined the CHN term in 2004 at a Telcordia symposium; now an Ericsson subsidiary.

CHN theory fully explains the movement from mainframe to PC to cloud. It explains the growth of switches, routers and data centers in networks over time. And it should be used as a model to explain how optical computing/storage in the core, fiber and MIMO transmission and cognitive radios at the edge get introduced and scaled. Mobile broadband and 7x24 access /syncing by smartphones are already beginning to reveal the pressures on a vertically integrated world and the need to evolve business models and strategies to centralized hierarchical networking.

*--interesting to note that creative destruction was original used in far-left Marxist doctrine in the 1840s but was subsumed into and became associated with far-right Austrian School economic theory in the 1950s. Which underscores my view that often little difference lies between far-left and far-right in a continuous circular political/economic spectrum.

A humble networking protocol 10 years ago, packet based Ethernet (invented at Xerox in 1973) has now ascended to the top of the carrier networking pyramid over traditional voice circuit (time) protocols due to the growth in data networks (storage and application connectivity) and 3G wireless.According to AboveNet the top 3 CIO priorities are cloud computing, virtualization and mobile, up from spots 16, 3 and 12, respectively, just 2 years ago! Ethernet now accounts for 36% of all access, larger than any other single legacy technology, up from nothing 10 years ago when the Metro Ethernet Forum was established.With Gigabit and Terabit speeds, Ethernet is the only protocol for the future.

The recent Ethernet Expo 2011 in NYC underscored the trends and importance of what is going on in the market.Just like fiber and high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2).This graphic illustrates why it has spread through the landscape so rapidly from LAN to MAN to WAN.With 75% of US business buildings lacking access to fiber, EoC will be the preferred access solution.As bandwidth demand increases, Ethernet has a 5-10x price/performance advantage over legacy equipment.

Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology).The graphic below shows how the growing horizontalization is supported by vertical integration of information (ie exchanges) that will make Ethernet truly “on-demand”.This model is critical because of both the variability and dispersion of traffic brought on by both mobility and cloud computing.Already, the underlying layers are being “re”-developed by companies like AlliedFiber who are building new WAN fiber with interconnection points every 60 miles.It will all be ethernet.Ultimately, app providers may centralize intelligence at these points, just like Akamai pushed content storage towards the edge of the network for Web 1.0.At the core and key boundary points Ethernet Exchanges will begin to develop.Right now network connections are mostly private and there is significant debate as to whether there will be carrier exchanges.The reality is that there will be exchanges in the future; and not just horizontal but vertical as well to facilitate new service creation and a far larger range of on-demand bandwidth solutions.

By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.It is consistent with my own definition of web 1.0 as a 4 layer stack.Replace layer 4 with clouds and mobile and you get the sense for how much greater complexity there is today.When you compare it to the above charts you see how far Ethernet has evolved in a very rapid time and why companies like Telx, Equinix (8.6x cash flow), Neutral Tandem (3.5x cash flow) will be interesting to watch, as well as larger carriers like Megapath and AboveNet (8.2x cash flow).Certainly the next 3-5 years will see significant growth in ethernet and obsolescence of the PSTN and legacy voice (time-based) technologies.

coverage is the next wave in LTE networks. Here’s a good video explaining AC in

coverage is the next wave in LTE networks. Here’s a good video explaining AC in  Cassidy Shield of Alcatel-Lucent, further stated that

Cassidy Shield of Alcatel-Lucent, further stated that  But with a strong message to the markets in Washington DC on March 11 from

But with a strong message to the markets in Washington DC on March 11 from

I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice.

I first started using clouds in my presentations in 1990 to illustrate Metcalfe’s Law and how data would scale and supersede voice. theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many.

theory needs to capture the dynamic of new service/technology introduction that initially is used by a small group, but then rapidly scales to many. d high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2).

d high-capacity wireless (MIMO) in the physical layer (aka layer 1), Ethernet has significant price/performance advantages in transport networks (aka layer 2). Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology).

Ethernet is getting smarter via a pejoratively coined term, SPIT (Service Provider Information Technology). By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.

By the way, I found this “old” (circa 2005) chart from the MEF illustrating what and where Ethernet is in the network stack.